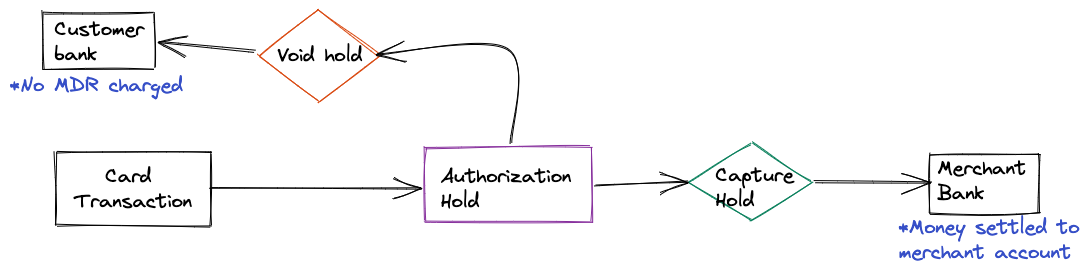

Pre-authorization (pre-auth) allows merchants to temporarily block funds on a customer’s card or account and capture the payment later, typically after order fulfilment. This helps secure funds without charging the customer immediately. Cashfree Payment Gateway (PG) supports pre-auth for UPI and for Visa and Mastercard credit, debit and prepaid cards.Documentation Index

Fetch the complete documentation index at: https://cashfreepayments-d00050e9-handbook-faq-creation.mintlify.app/llms.txt

Use this file to discover all available pages before exploring further.

How pre-authorization works

Pre-authorization allows you to manage payments flexibly in the following ways:- Authorise an amount on a customer’s card or account without immediate capture.

- Capture the authorized amount later—either fully or partially—when required.

- Void the authorisation to release the blocked funds if the order is not fulfilled.

Pre-authorization flow

- The customer initiates the payment.

- The amount is blocked on the customer’s card or account after successful payment completion.

- The merchant can:

- Either Capture the full or partial amount.

OR - Void the authorisation to release the blocked funds to the customer.

Pre-authorization feature request

Managing pre-authorization transactions

You can capture or void pre-auth transactions from the Cashfree Merchant Dashboard or integrate the capture and void APIs to automate the process.- You must capture or void a pre-auth transaction within seven days of authorisation.

- A transaction can only be captured or voided once.

- Once captured, a transaction cannot be voided.

- Once voided, a transaction cannot be captured.

- Transactions not captured within 7 days are automatically released back to the customer.

- Voided transactions return funds to the customer immediately.

- After pre-auth is enabled for your account, ensure all Pre Auth transactions are either captured or voided.

Supported payment instruments for pre-authorisation

Cashfree Payment Gateway supports pre-auth workflow on cards and UPI (Unified Payments Interface).Cards

Once Pre-Auth is enabled for your account, every card payment will be Pre-Auth by default, you do not need to provide any additional parameters while initiating the payment. Below is a sample Order Pay API request and response:UPI

For UPI pre-auth, you need to pass additional parameters in the/orders/pay API request. Once you have created the order, invoke the Order Pay API call with the authorize_only, authorization parameters.

The authorization object contains the following attributes:

approve_by- The time by when customer needs to approve this one time mandate request.start_time- The time when the mandate should start.end_time- The time until when the mandate hold will be on customer’s bank account. You can call capture and void until this time.

UPI Collect

Below is a sample UPI Collect request and response:UPI Intent

Below is a sample UPI Intent request and response:Capture

The capture workflow helps you to capture the payment and move the authorised amount partially or completely from customers bank account to your bank account, by calling Pre-Authorization API for capture.Void

The void workflow helps you to release the entire authorized amount back to the customer, by calling Pre-Authorization API for void.FAQs

What is a capture call in Pre-Authorization?

What is a capture call in Pre-Authorization?

What is the validity of capture?

What is the validity of capture?

Can a merchant capture a partial amount?

Can a merchant capture a partial amount?

Is MDR charged on the authorized or captured amount?

Is MDR charged on the authorized or captured amount?

Which cards support pre-authorization?

Which cards support pre-authorization?

What is void in Pre-Authorization?

What is void in Pre-Authorization?

Can a merchant void a partial amount?

Can a merchant void a partial amount?

What are some common use cases for Pre-Authorization?

What are some common use cases for Pre-Authorization?

Is pre-authorization feasible via payment links and payment forms?

Is pre-authorization feasible via payment links and payment forms?

How does settlement occur in a pre-authorization transaction?

How does settlement occur in a pre-authorization transaction?

When does the merchant receive the funds in a pre-authorization transaction?

When does the merchant receive the funds in a pre-authorization transaction?

What happens if a customer disputes a settled transaction?

What happens if a customer disputes a settled transaction?

Is the pre-authorization feature supported on American Express and Diners cards?

Is the pre-authorization feature supported on American Express and Diners cards?